South African agriculture is moving into the next production cycle with two realities sitting side by side. The first is encouraging: grain and oilseed supplies are far healthier than they were in tighter seasons, and that gives the market more breathing room. The second is less comfortable: the climate signal is becoming more uncertain, and that uncertainty matters for every major decision from wheat planting in the winter rainfall region to maize, soybean and sunflower planning in the summer crop belt.

When ABSA AgriTrends Autumn 2026 is read alongside Wandile’s agricultural market viewpoint and the latest Grain SA reports, the message is not one of fear. It is one of caution, timing and discipline. South Africa is not entering a season with no upside. It is entering a season where farmers may need a more strategic reading of weather, crop mix, planting windows and risk.

South Africa has a stronger market base than it had before

One of the most important starting points for the next cycle is that the grain market is not entering this period from a position of immediate supply stress.

Grain SA’s March 2026 projections show total maize area for 2026/27 at 2.716 million hectares and expected production at 16.508 million tonnes. White maize is projected at 1.645 million hectares and 8.758 million tonnes, while yellow maize is projected at 1.072 million hectares and 7.75 million tonnes. Soybeans are projected at 1.213 million hectaresand 2.73 million tonnes.

That matters because it changes the tone of the season. In years when stocks are tight, producers often feel pressure to chase output aggressively. In a year with more comfortable supply, the conversation shifts. Profitability, risk exposure, crop suitability and regional conditions start to matter more than simple volume. South Africa is going into this period with a better commercial buffer than it had in more pressured years, and that gives farmers a little more room to think carefully rather than react emotionally.

Still, stronger stocks do not remove weather risk. They only soften the blow if the weather becomes difficult. In that sense, the market cushion is stronger, but the climate cushion looks weaker.

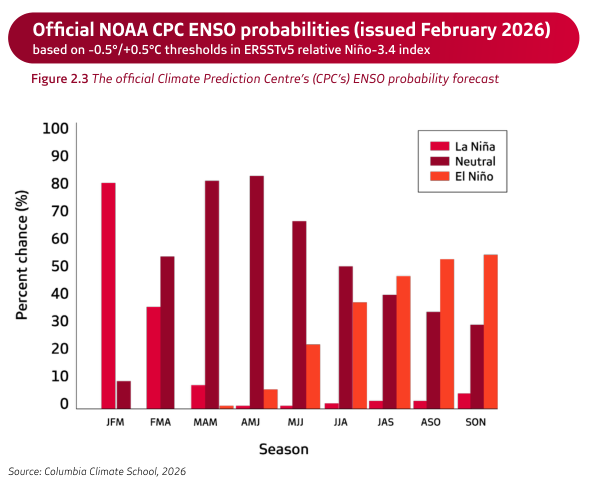

The climate signal suggests a more difficult production environment ahead

The broad climate picture from ABSA AgriTrends Autumn 2026 and Wandile’s agribusiness view suggests that South Africa may be heading away from the relatively supportive setup that helped parts of the recent season and toward a more difficult 2026/27 summer pattern.

For farmers, that matters less as a theoretical climate debate and more as a farm-business question. If rainfall becomes less dependable later in the season, the biggest losses often do not come from obvious early failure. They come from crops that establish well and then run into stress during flowering, pod fill or grain fill.

That is why the next season demands more strategic thinking. The key issue is not just whether planting rain arrives. The key issue is whether crops can carry enough moisture support through the most sensitive growth stages.

Summer rainfall region: the season may become tighter as it progresses

In the traditional summer rainfall areas, including the maize, soybean and sunflower belt, the main risk is that the season could open reasonably and then become hotter or drier as it matures.

That pattern matters most in the western side of the summer grain belt. Areas in the North West and western Free State generally have less room for error when rainfall breaks are longer and temperatures rise. By contrast, eastern production zones such as Mpumalanga and stronger soybean districts often hold a slightly better moisture advantage, although they are not immune when the season turns.

This is where crop planning becomes a form of strategic discipline. Not every hectare should automatically be treated the same. Better soils, stronger moisture profiles and historically dependable planting windows can justify more confidence. Marginal land under uncertain moisture may not.

Maize outlook: still central, but not equally safe everywhere

Maize will remain the backbone of the summer crop economy. That is not changing. What may change is how confidently producers place maize in riskier zones.

Grain SA’s figures show a sizeable maize crop and strong commercial supply. Total commercial maize supply is projected at 18.641 million tonnes, with exports at 5.109 million tonnes.

From a market point of view, that is a useful reminder that South Africa is not planting into panic. But from a farm point of view, it also means that aggressive maize expansion on weaker land may be harder to justify if the weather outlook turns against those hectares.

For producers in the stronger eastern belt, maize should remain a rational option where fertiliser budgets, hybrids and planting dates align. In drier western zones, however, the maize decision may become more selective. That does not mean farmers should abandon maize. It means maize becomes a more strategic call, especially where yield risk rises sharply if rains fade after establishment.

Soybeans: still attractive, but weather timing remains crucial

Soybeans continue to hold one of the strongest structural stories in South African row-crop farming.

Grain SA projects soybean production at 2.73 million tonnes, with total commercial demand at 2.694 million tonnes, supported strongly by domestic crushing.

That matters because soybeans are not simply a weather gamble. They sit inside a broader processing and demand structure that keeps them commercially relevant. In the eastern Free State, Mpumalanga and other higher-potential soybean zones, the crop should remain a sensible part of the rotation.

But soybeans are not protected from climate stress. If heat and moisture pressure hit at flowering or pod fill, the crop can lose momentum quickly. That is why soybeans should be treated as a crop with upside, but not as a guaranteed answer. On the right farms, soybeans remain highly attractive. On the wrong farms, in the wrong timing window, they become less forgiving than many assume.

Sunflower: the quiet insurance crop of the next strategic cycle

If one crop could gain importance quietly but meaningfully, it is sunflower.

In a more uncertain summer rainfall season, sunflower often returns to the centre of conversation because it gives producers flexibility. It can make sense where farmers want to reduce exposure, where planting dates become awkward, or where confidence in late-season moisture weakens.

That could make sunflower a highly strategic crop in 2026/27. It may not dominate the national conversation in the same way maize does, but in western and lower-potential production areas it could become one of the smartest tools available for balancing risk.

Sunflower’s importance in such a season is not just agronomic. It is psychological. It gives farmers an option when confidence drops. In uncertain years, having a credible fallback can be just as important as chasing the highest possible upside.

Winter rainfall region: wheat depends on timing, not assumptions

The winter rainfall region has to be read on its own terms. The logic that applies to the summer grain belt cannot simply be copied and pasted onto the Western Cape and other winter wheat areas.

For wheat, rainfall distribution matters as much as total rainfall. A season can still perform respectably if the opening rains arrive in time, crops establish evenly and follow-up fronts support the crop through key developmental stages. On the other hand, a season with uneven rainfall timing can disappoint even if headline totals do not look disastrous.

That means the winter crop season should be approached with a strategic mindset rather than a fixed expectation.

Wheat outlook: important, exposed and still highly relevant

Wheat remains one of the most important crops in the national food picture, and South Africa still relies on imports to bridge the gap between domestic production and demand.

Grain SA projects wheat area at 517,300 hectares and production at about 1.897 million tonnes for the 2025/26 marketing season, while imports are still expected at roughly 1.76 million tonnes.

That tells farmers two things. First, local wheat still matters enormously. Second, the country does not have much reason to be casual about local wheat performance.

For wheat producers, the broad outlook is workable but weather-sensitive. If winter rainfall patterns cooperate and fronts are spaced well enough, the crop can still deliver a respectable result. If the season becomes patchy, the pressure rises fast. Wheat therefore becomes a crop where strategic management of timing, costs and planting windows may matter more than broad seasonal optimism.

The honest national outlook for planting and harvesting

So what should farmers and meteorologists say, in plain language, about what lies ahead?

The most honest answer is this:

South Africa is moving into a season that may reward calm judgment more than confidence.

The winter rainfall regions do not yet look like a write-off, but they do look vulnerable to rainfall distribution problems. Wheat producers should prepare for a season where establishment and follow-up rain both matter.

The summer rainfall regions look more exposed than the season just passed. The risk is not simply that the season starts badly. The risk is that it starts adequately and then tightens later, especially across western areas where moisture margins are already thinner.

Maize remains the anchor crop, but not every hectare deserves the same confidence. Soybeans remain commercially attractive, especially in stronger eastern zones. Sunflower may become the most useful balancing crop in drier regions if planting conditions lose momentum.

That is why 2026/27 is best understood as a strategic forecast, not a dramatic one. There is no strong case for panic. There is also no case for lazy optimism.

What smart farmers may do differently this season

The next production cycle may reward producers who make slightly sharper decisions earlier.

That could mean:

- placing maize more selectively in western regions

- protecting soybean exposure for better rainfall zones

- keeping sunflower ready as a flexible option

- treating wheat as a timing and moisture management exercise rather than a routine seasonal programme

- building budgets around downside protection, not only best-case yield expectations

In a season with stronger market supply but a trickier weather profile, the biggest edge may not come from predicting every rainfall event. It may come from reducing avoidable mistakes.

That is where the real strategic advantage lies.

Final word

South African farming is not heading into a season without promise. The country has stronger grain supplies, better market visibility and more room to absorb shocks than it had in tighter periods. But it also appears to be heading into a more uncertain weather phase, especially for the next summer crop cycle.

For farmers, that means the old rule still holds true: seasons are not won only by weather. They are won by preparation, crop fit, timing, discipline and strategic decisions.

The farmers who perform best in 2026/27 may not be the ones who make the boldest choices. They may be the ones who make the most strategic ones.

10 Questions and Answer

1. What is South Africa’s farming outlook for 2026/27?

It looks like a more strategic season, with better grain supplies in the system but more weather uncertainty ahead, especially for summer crops.

2. Will weather risk increase for South African farmers in 2026/27?

Yes. The broad signal suggests a less comfortable climate setup than the one that supported the stronger recent summer crop. It is time for strategic decisions

3. Which areas are most exposed in the next summer season?

The western side of the summer rainfall belt, including drier parts of the North West and western Free State, appears more exposed if the season turns hotter and drier and will call for strategic thinking.

4. Is maize still a good option for 2026/27?

Yes, but not every maize hectare carries the same level of safety. Higher-potential zones still support maize best.

5. What is the soybean outlook for South Africa?

Soybeans remain attractive, especially in stronger eastern production zones where domestic crushing demand supports the crop.

6. Could sunflower become more important in 2026/27?

Yes. If summer planting conditions become uncertain, sunflower may become more valuable as a lower-risk balancing crop.

7. What is the wheat outlook for the winter rainfall region?

The outlook is workable, but highly sensitive to rainfall timing and distribution. Wheat remains important because South Africa still relies heavily on imports.

8. Are grain supplies currently stronger than before?

Yes. Grain SA’s latest projections show a much more comfortable maize and soybean supply picture than in tighter seasons.

9. What should farmers monitor most closely before planting?

Opening rainfall, subsoil moisture, heat risk later in the season, and whether each crop still makes sense on each farm under current cost pressure.

10. What is the best approach for 2026/27?

A strategic approach: match crop choice, planting windows and input exposure to realistic regional weather risk rather than assuming the next season will behave like the last one.